View

Video

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

When you invest in UK smaller companies, also known as small caps, you are backing young, dynamic UK companies that are often highly innovative, with the agility to adapt quickly to seize on emerging business opportunities.

The growth prospects of these smaller companies can dwarf those of the FTSE 100 giants and, because there are fewer fund managers and analysts studying this end of the market, this potential can often be overlooked. This creates opportunities for large and experienced teams like ours to spot potential winners before others do.

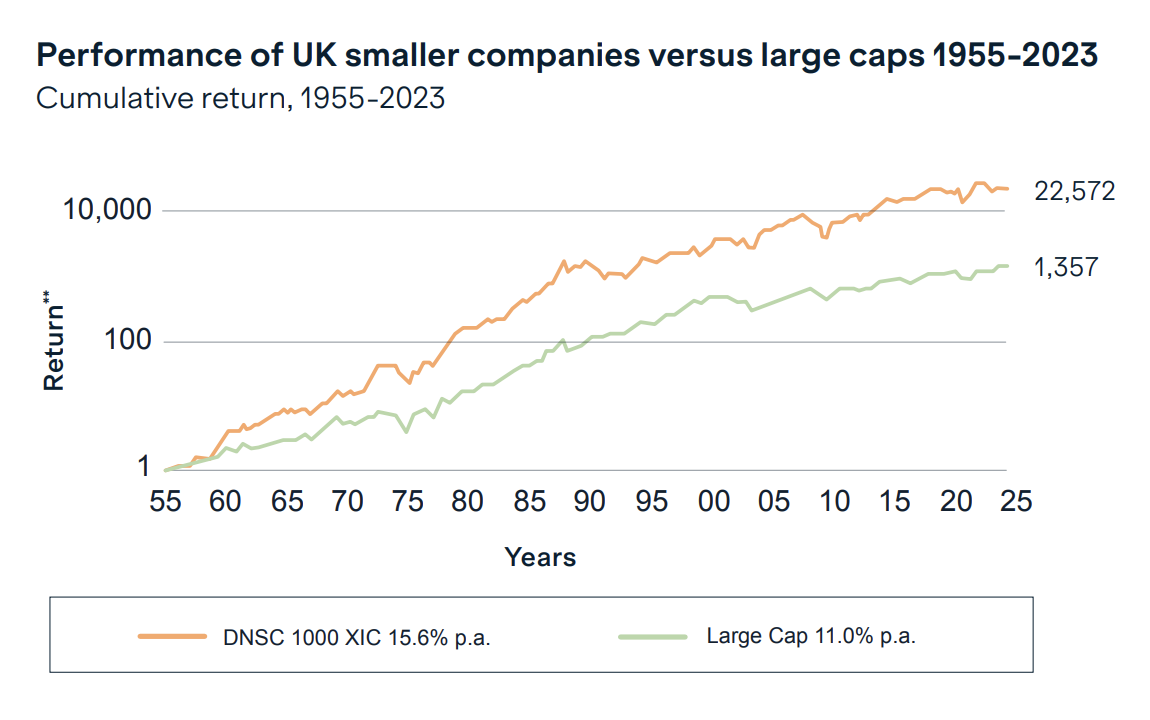

Historically, the shares of UK smaller companies have significantly outperformed those of their larger counterparts over the long term, as the chart below shows.

The Deutsche Numis Smaller Companies 1000 index consists of the bottom 2% of companies by stock market value on the main UK stock market. This index returned annualised growth of 15.6% over the 69 years from 1955 to 2023*. This compares with a return equivalent to 11% a year by the UK’s largest listed companies, as represented by the Deutsche Numis Large Cap Index, over the same period.

Past performance is no guarantee of what will happen in the future, of course. It is also worth remembering small caps can be more sensitive to economic headwinds and their share prices can move sharply, for example, when a business runs into trouble. One of the benefits of investing through a fund holding a spread of companies is that it helps to manage this stock-specific risk. We currently have just over 160 stocks in our portfolio.

We believe there is a particular opportunity, with UK small-cap stocks looking, in our view, significantly undervalued. These smaller companies have experienced a challenging period, with central banks around the world countering high inflation with the most aggressive interest rate raising cycle of the past 40 years*.

We have also seen war return to Europe, with Russia’s invasion of Ukraine causing steep increases in energy prices, and the UK has experienced a tumultuous period in politics, with 2022 seeing three different prime ministers and four Chancellors of the Exchequer.

However, interest rates now appear to be falling, inflation is close to the Bank of England’s 2% target and the UK government, which was elected with a large majority, seems to have brought a degree of political stability.

While UK small caps have been out of favour with global investors for a number of years, we see signs that this may be changing. In November, after more than three years of money flowing out of funds investing in UK shares, the direction of travel reversed and there were net flows of more than £300m into these funds (source: Financial Times, 4th December 2024).

There is also an increase in merger and acquisitions activity, with rival companies and private equity houses clearly seeing value in UK companies at current valuations. In our own fund, over the past 12 months we have seen bids for companies including Aquis Exchange, Eckoh, Loungers, Centamin, IQ Geo, Mattioli Woods, Alpha Financial Markets Consulting, GRC International, TClarke, FireAngel Safety Technology, Shanta Gold and Kin & Carta.

As stock-pickers, we see UK small caps as a fertile hunting ground, and we hold a portfolio broadly diversified across a range of business sectors. Of course, there are areas we tend to avoid, such as the biotech sector, where outcomes tend to be binary and in-depth specialist knowledge is required. We are also less enthusiastic about sectors such as retail and hospitality, after measures announced in the Budget pushed up their staffing costs.

Beyond these areas though, we see opportunities in everything from tech companies to telecommunications and the industrial sector. Many of the businesses we hold are ‘growth’ stocks – companies forecast to achieve strong earnings growth, and on higher valuations as a result. The share prices of a lot of these companies have suffered as interest rates have risen. This is partly because, if rates are higher, consumers are likely to spend less, hitting long-term profits. On the flip side, with rates now falling, we see good reasons to believe that these companies can reap the benefits.

Five high-growth companies we hold are Alpha Group International, which provides companies with foreign currency services; Beeks Financial Cloud Group, which provides a cloud-based platform connecting financial institutions; Boku, which provides payment services via mobile phones; Filtronic, which makes components for telecoms systems and satellites; and Trustpilot, which is a global reviews platform.

In combination, these five companies have projected they will grow their revenues by 22% and their profits by 35% each year between 2024 and 2026**. This is not guaranteed, and investing in smaller companies is not without risk, of course, but we believe these businesses are strongly positioned to outperform as rates continue to fall and investors take a fresh look at their growth potential.

We are also seeing attractive opportunities among gold and silver miners, and in some classic ‘value’ stocks, companies that look undervalued at their current share price. In our fund, these include Stelrad Group, a leading manufacturer of radiators; and Norcros, which is a UK market leader in showers and bathroom furnishings.

Currently, we believe UK small caps look undervalued in absolute terms, in comparison with similar companies listed on other stock markets and relative to their own historical averages. We do not think they will remain this cheap indefinitely. We believe that taking a long-term view, current valuations represent a highly attractive opportunity.

*Source: The Guardian https://www.theguardian.com/business/2023/jul/26/fed-raises-interest-rates

**Sources: companies' own projections and investment team's analysis'.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.