View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

Last week, after our weekly five-a-side game, a few of us stayed behind for the usual post-match debrief. As is traditional, the football improved with every retelling, and the claims about missed chances became increasingly outrageous.

The conversation naturally turned to the World Cup. Who will win? Will France do it again? Have Spain become the team to beat? How do things look for England and Scotland? What about some of the other teams, like South Africa?

The discussion reminded me of a recent article by Financial Times columnist Simon Kuper, who observed with admirable frankness that nobody really knows. He then went into considerable detail explaining why.

Football is an unusually unpredictable sport. A lower-ranked team can defend for 90 minutes, nick a goal, win a penalty shootout and send a favourite packing. Unlike many sports, the best team doesn’t always win.

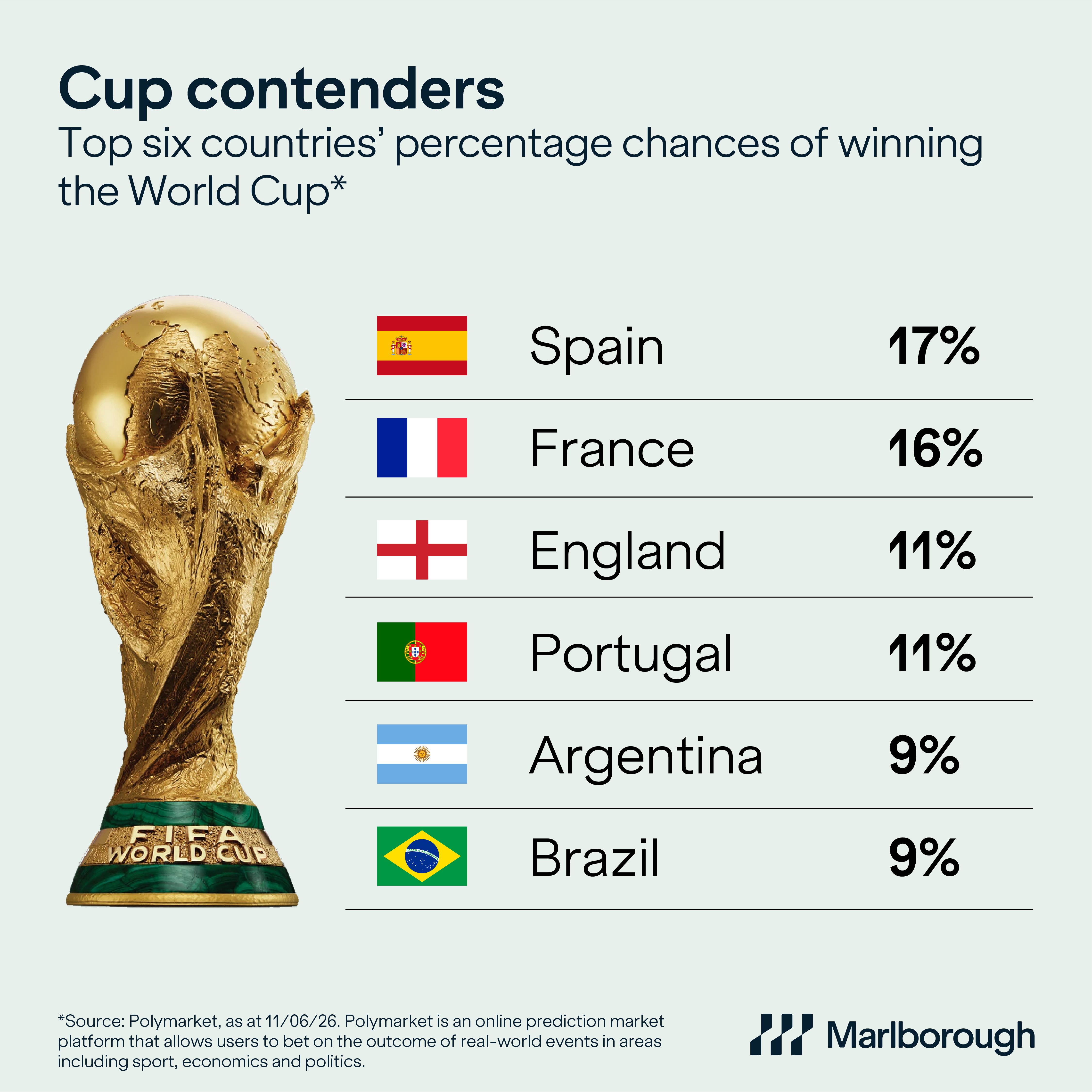

Kuper’s conclusion was that France and Spain are probably the most likely winners, with England, Portugal and Brazil not far behind.

Our chart this week expands on this theme and shows the chances of different countries winning the World Cup, based on bets by clients of Polymarket. This is an online prediction market platform that enables users to bet on the outcome of real-world events in areas such as sport, economics and politics.

They take a similar view to the FT’s Kuper on the teams most likely to succeed, although they also believe Argentina are in with a decent chance.

The fact that opinion is so divided underlines just how difficult it is to forecast who will come out on top this time. Individual star players, squad depth and tactical flexibility are all key considerations. In addition, a range of other factors such as group composition and injuries add further layers of unpredictability.

It struck me that this isn’t entirely different from investing.

We spend countless hours analysing data, studying economic forecasts and assessing probabilities. Ultimately, however, even the most experienced and astute investor can’t predict for certain which asset class will outperform over any given time period.

This highlights the key benefit of multi-asset investing. The goal isn’t to know exactly what will happen. It’s to sensibly position our portfolios for a range of outcomes.

We do this by building broadly diversified portfolios comprised of a range of different asset classes. By having exposure to, for example, US equities*, European equities, emerging market equities and government bonds** the intention is to increase the opportunities for growth, while helping to manage risk.

As multi-asset investors, we believe a sensible long-term approach is to hold a carefully balanced blend of equities – with exposure to a range of different stock markets – and bonds. Equities can be viewed as aggressive attackers intended to drive growth, while bonds are the disciplined defenders intended to protect a portfolio.

Ultimately, the nation that brings home the World Cup won’t win just because of its star players. Success will depend on the complementary skills, cohesion and tactical flexibility of the whole team.

We apply the same principle to multi-asset investing. We carefully blend assets with a range of different characteristics into portfolios designed to navigate evolving market conditions and help investors achieve their financial goals over the long term.

*Equities are company shares.

**Bonds are interest-paying financial products issued by governments, companies and other institutions when they want to borrow money from investors.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.