View

The Bond Bulletin

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

It is said that nothing is certain except death and taxes. But I am minded to suggest a third certainty: ‘sell-side’ strategists being bullish on equities in their annual year-ahead outlook pieces.

These are the strategists working at banks and brokerages, the companies who sell securities, products and services to asset managers and investors such as myself – the ‘buy side’.

To a significant degree a bullish perspective is understandable. Firstly, because they have products to sell. It is harder to convincingly sell equities to clients when your strategy team is out there calling for them to decline in price. More cynically, the bullish bias is justifiable on the basis that history says equities will go up a lot more than they go down. Not in magnitude per se (at least not consistently and persistently from all starting points), but in frequency. In broad strokes it is true that equities are likely to rise in price about 10 times as often as they decline in price across an entire calendar year. So, if you just play the odds, it makes sense to always be bullish. Furthermore, there may be some game theory involved. If all (or at least most) other strategists are bullish, then sticking your neck out to expound a bearish theory, however well thought out, is a bit of a career risk. As John Maynard Keynes put it: “Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally”. Play politics, play the odds and play the game.

As a group, we fixed income investors are always a little less ‘glass half full’ than our equity counterparts. That does not mean that we are all perma-bears of course, although sometimes it may feel like it. It is the inevitable result of investing in securities with asymmetric downside. In bonds, there is a limit to how much you can gain, since interest payments are fixed. But if things go wrong – like a default – then potentially you can lose significantly more.

If I were being honest, I would say it is often also the inevitable result of actually looking under the economic hood. However, I refuse to go down that rabbit hole so close to Christmas… no bah humbug from this Ebeneezer Bond!

Instead, I am just going to pick out a few interesting thoughts and observations concerning the year ahead, to provide some food for thought for those who want to think a little more deeply.

1. Price is what you pay, value is what you get. The same prima facie, unqualified, statistical, historical analysis which tells us that stocks go up more frequently than they go down also tells us that buying US equities at these sorts of valuations is likely to lead to meagre long-term returns. Outside of the US you can still pick up reasonably valued securities in reasonably valued markets. Some of them even allow you to play the ‘AI is changing the world trade’.

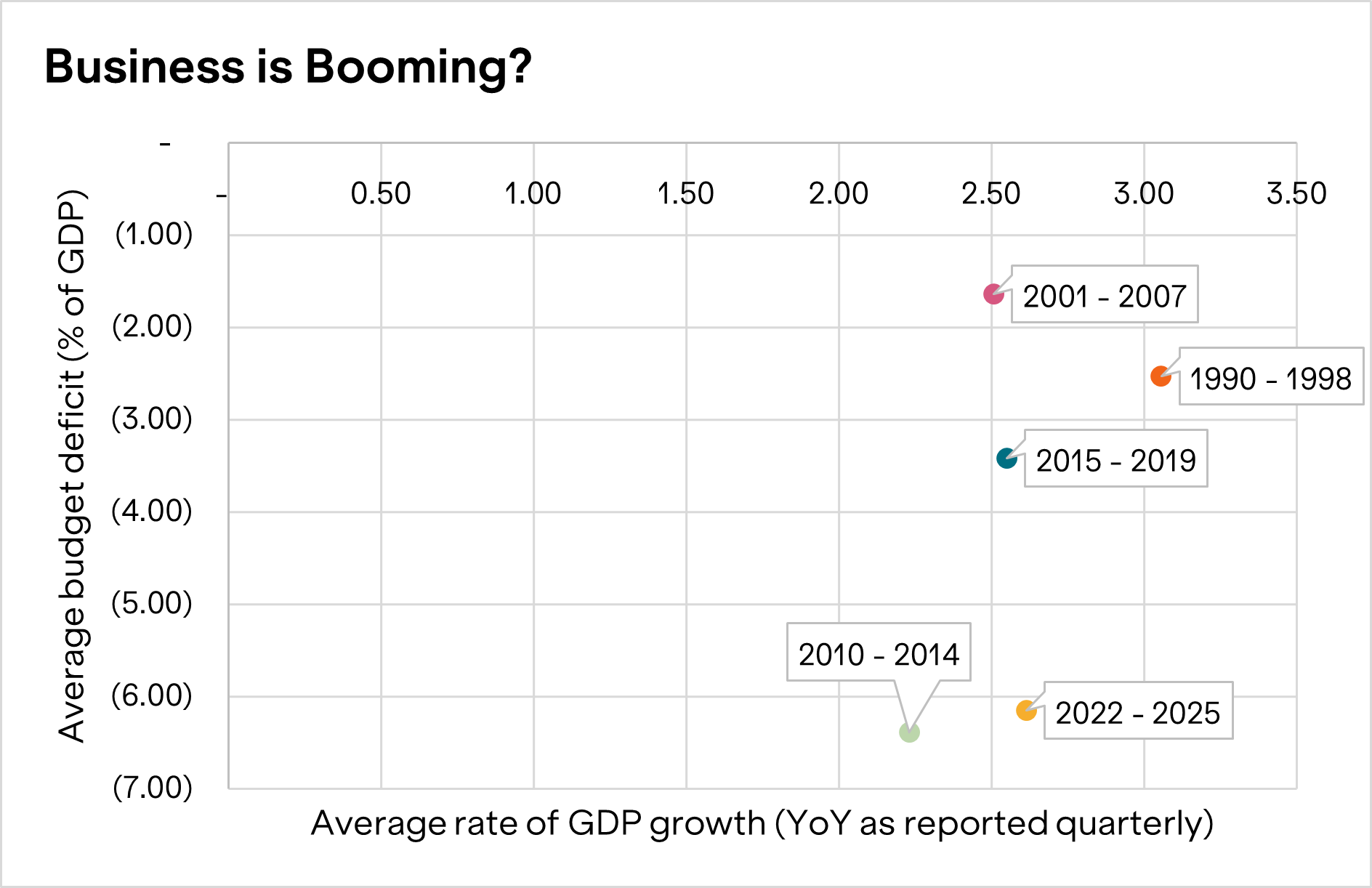

2. If the US economy is so strong, then just why does it need so much support from the US government? The scatter plot below shows that since the end of the 1990s it has mostly taken more and more government deficit spending to produce the same GDP growth outcomes. What happens if the government changes course? Or is forced to change course?

3. Diversification is beneficial and desirable only to the extent that there is low correlation between the returns of the assets in a portfolio. If all the assets in your portfolio always go up and down together, regardless of which asset class they are in, then it is likely you are not well diversified.

4. Do not allow broad-brush labels to sway you away from objectively attractive investments. Under the banner of ‘emerging markets’ there are attractively priced and fundamentally supported assets. In many cases, particularly since COVID, it us the supposedly ‘developed’ markets where the worst economic and policy making behaviour can be found.

5. You do not need to be a contrarian to be a successful investor. In fact, the prevalence of systematic investment styles in modern markets has made it harder and harder to be a contrarian – momentum has become the new gravity. That does not mean the rules of investing have completely changed though. And it certainly does not mean that always doing what worked last time will yield positive results. In the end, prices go up when buyers are more motivated and/or larger in terms of their financial footprint. Likewise with respect to sellers and a falling market. An exhaustion of buyers or sellers is as likely to mark a turning point as a change in the fundamentals. Particularly when fear or greed are in charge.

I should emphasise that I am not offering predictions or answers, just sharing how we think in the Marlborough fixed income team. We want to consider the ‘what ifs’ as well as the ‘most likelies’. We want to ask deeper questions, challenge all thinking – especially consensus – and then ultimately invest where we believe we are being appropriately rewarded for the risks we face. It may be old fashioned, but in our opinion that is what investing is all about.

Thanks for taking the time to read our pieces this year. From all at Marlborough, we wish you a happy and healthy Christmas. See you in the New Year.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.