View

Video

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

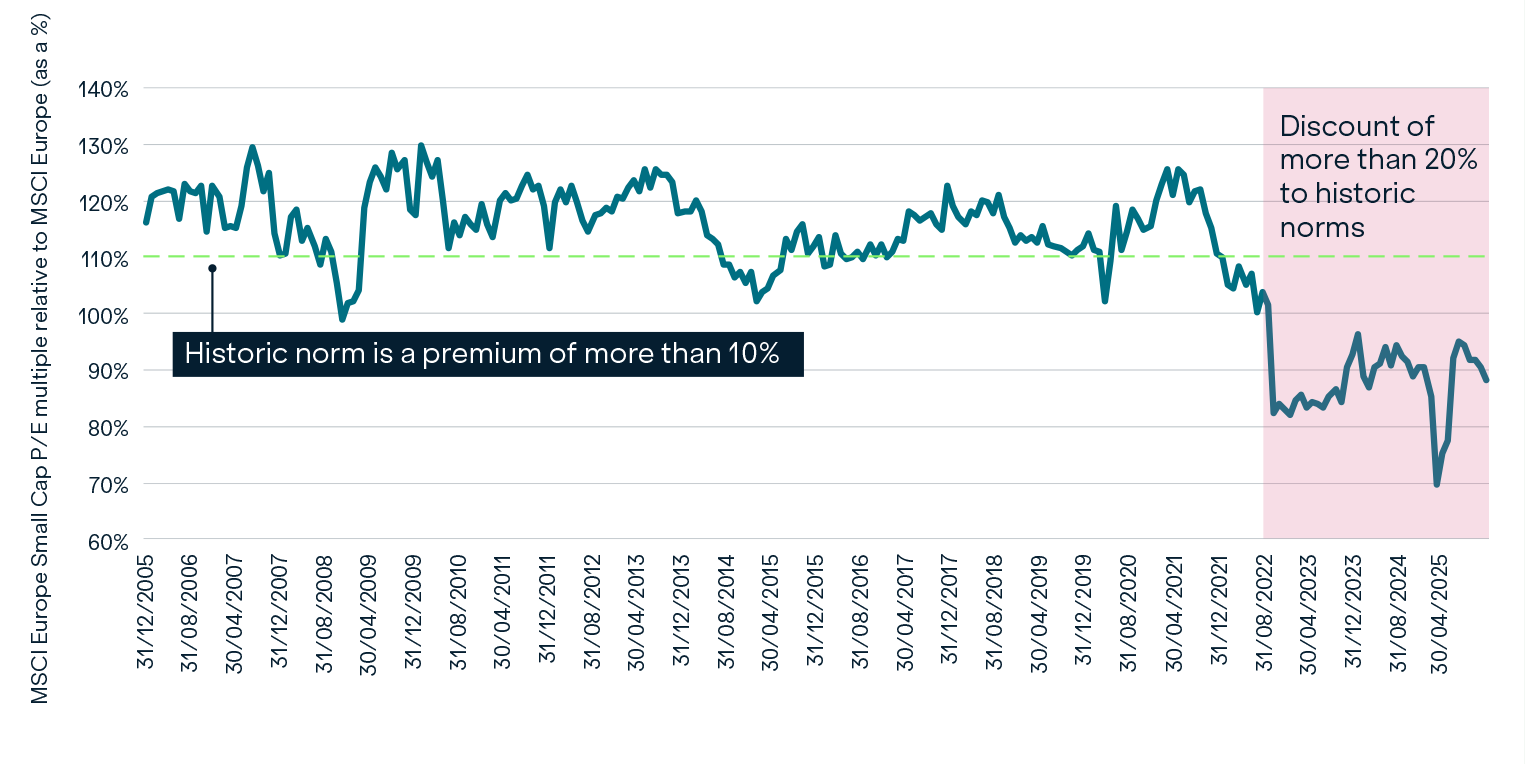

The superior long-term earnings growth potential of European small caps means they have historically traded on price-to-earnings (P/E) multiples significantly higher than their larger counterparts.

However, this long-term trend has been inverted since 2022. Based on P/E multiples, the MSCI Europe Small Cap Index is trading at a discount of more than 10% relative to the MSCI Europe Index, according to Bloomberg data. This is in stark contrast to data stretching back to 2005 that shows small caps typically trading at a premium of more than 10% relative to the MSCI Europe Index. It means European small caps are trading at a discount of more than 20% to historic norms.

P/E multiples of MSCI Europe Small Cap relative to MSCI Europe

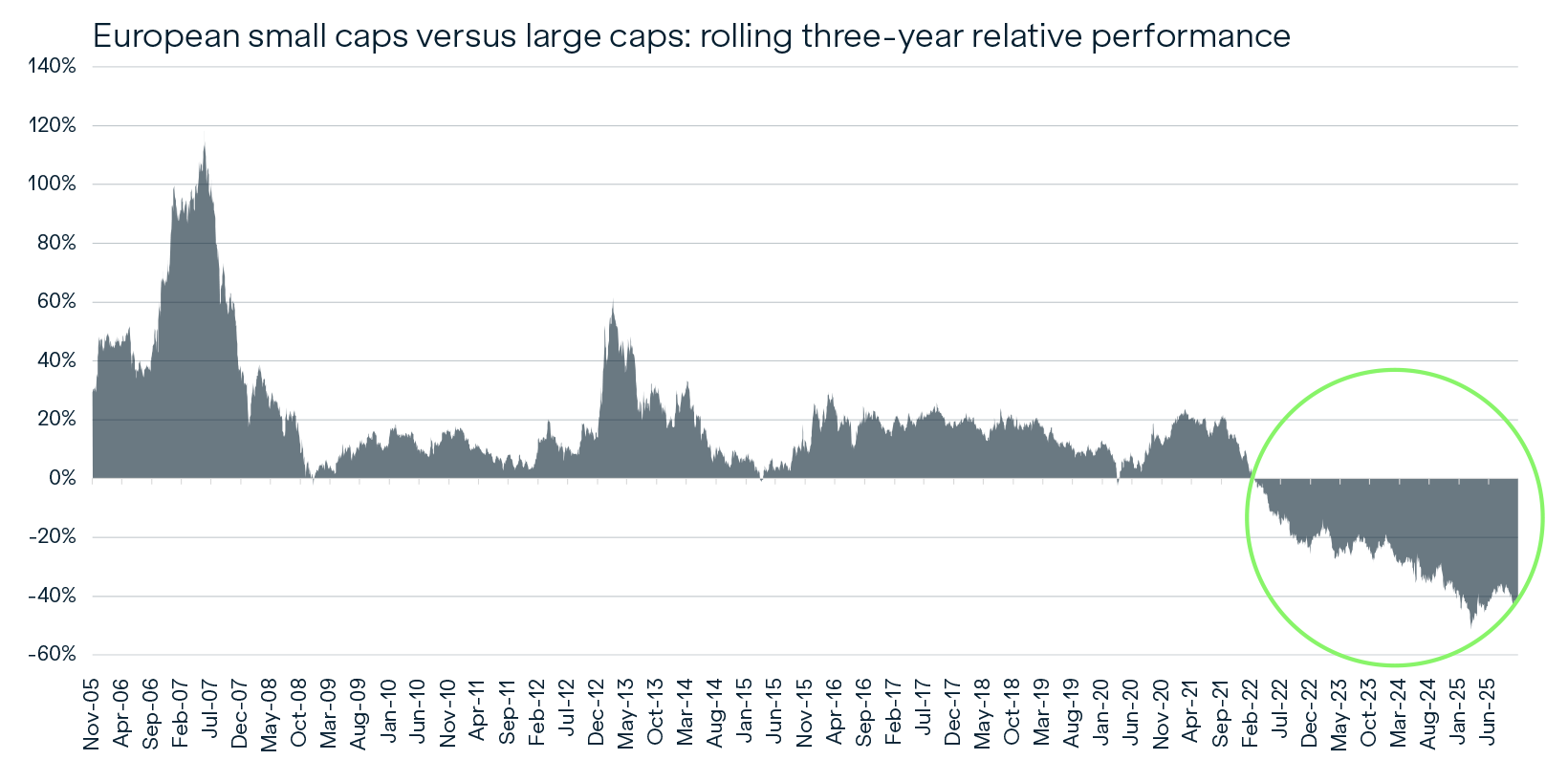

The valuation case is further reinforced by a comparison of the performance of European small caps versus large caps since the beginning of 2022. The chart below shows the rolling three-year relative performance of European small caps versus large caps. On this basis, European small caps are looking their cheapest relative to large caps in more than 20 years.

Small Caps looking cheapest for more than 20 years

This period of underperformance by small caps versus large caps is the result of a combination of headwinds. Higher interest rates tend to hit smaller companies harder. Macroeconomic uncertainty led investors to favour large companies with global exposure and stronger balance sheets.

In addition, strong performance by a number of European blue-chips boosted the performance of the large-cap index. However, we believe there are signs of the trend reversing and small caps beginning to outperform once more.

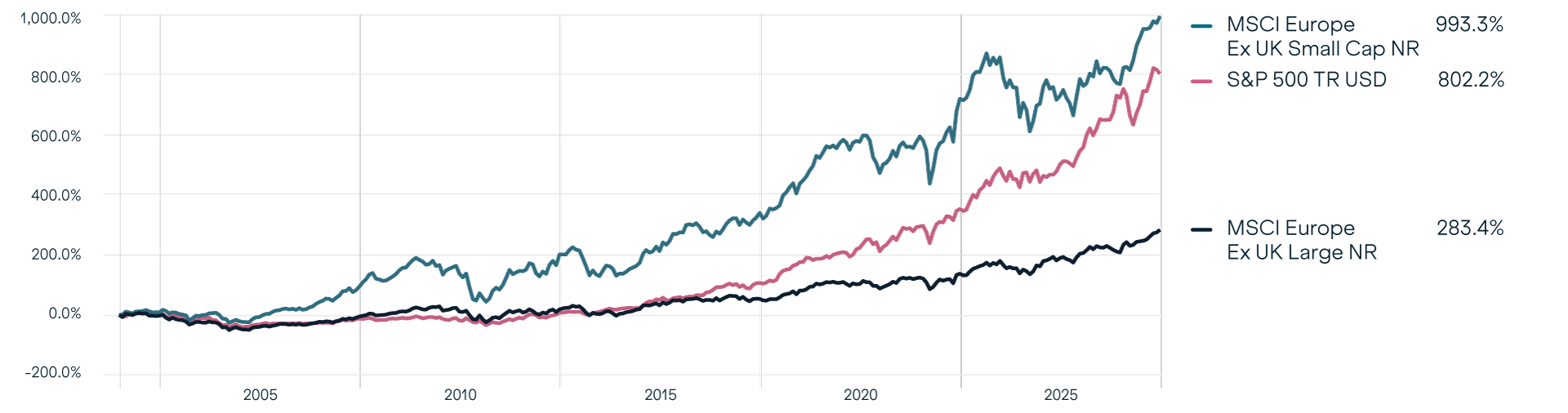

European small caps have an exceptional long-term performance track record. Between 01/01/2000 and 31/12/2025, the MSCI Europe ex-UK Small Cap Index returned 993% in sterling terms. Over the same period, the MSCI Europe ex-UK Large Cap Index was up 283%. It is notable that European small caps also outperformed the S&P 500, which returned 802% over the same period.

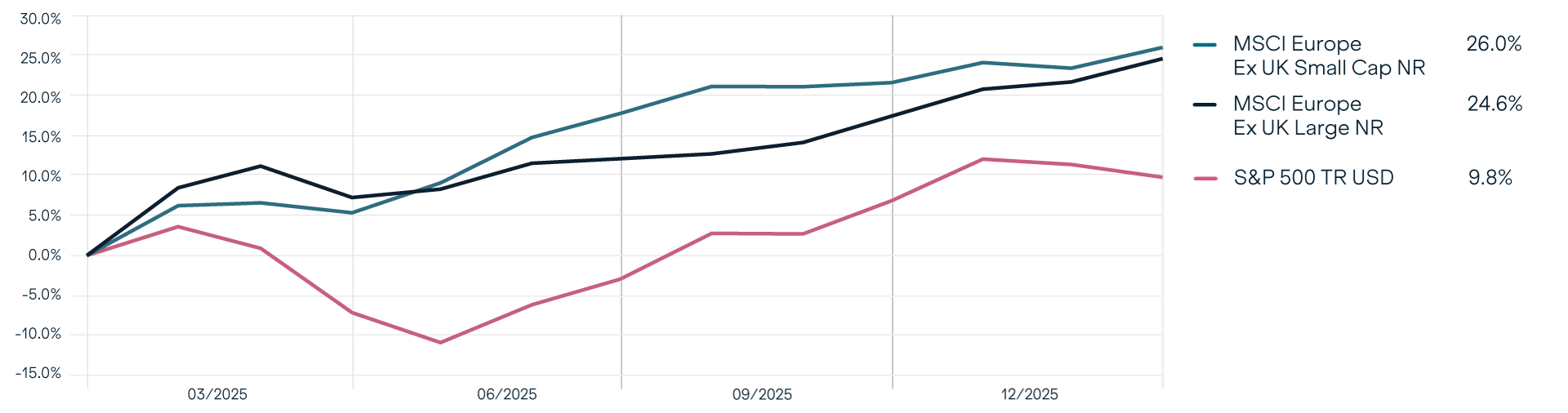

After a period of underperformance, this historic trend of small and micro-cap equities outperforming large caps may now be reasserting itself. During 2025, the MSCI Europe ex-UK Small Cap Index is up 26.0% and the MSCI Europe ex-UK Large Cap Index is up 24.6% (data to 31/12/25, all returns in sterling terms). It is interesting to note too, that over the same period the S&P 500 is up a comparatively modest 9.8% (see chart below).

This comes at a time when European equity funds are attracting inflows from UK investors, while other equity sectors are experiencing outflows.

Investors moved more than £200m into European equity funds in September 2025 – the fifth consecutive month of positive inflows, according to Calastone data.

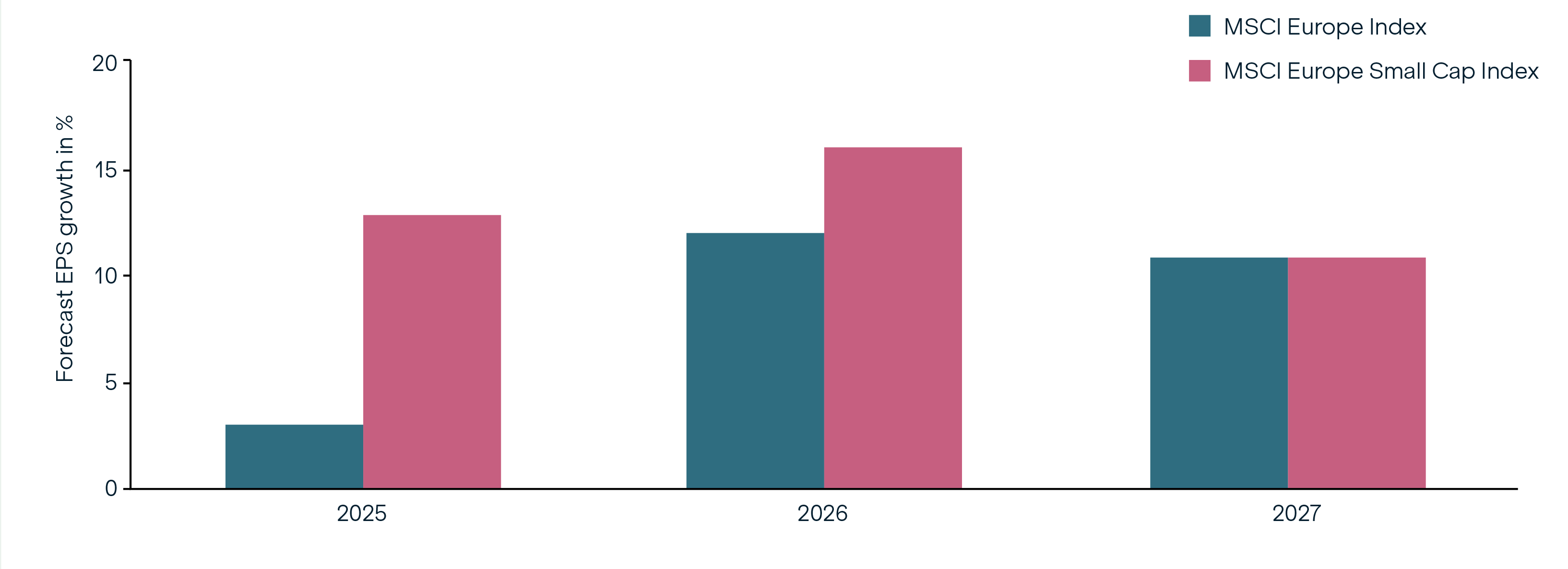

Against a backdrop of trade tariffs and geopolitical tensions, analysts downgraded earnings-per-share (EPS) forecasts around the world last year. However, European small caps saw only modest downgrades. The MSCI Europe Small Cap Index was still forecast to increase overall EPS by 13% year-on-year in 2025, according to State Street/FactSet data. Meanwhile, the MSCI Europe Index, comprised of larger companies, was only expected to achieve 2% EPS growth. Small cap EPS growth was forecast to outperform large caps again in 2026.

Many small-cap and micro-cap companies have characteristics that can enable them to achieve superior long-term growth potential compared to larger businesses.

• Innovative. Small and micro-cap companies are often innovators, bringing ground-breaking new products and services to market.

• Agile. In many cases, they can move more swiftly than their larger counterparts to seize new opportunities or adapt to regulatory change.

• Longer growth runway. Businesses at an earlier stage in their life cycle have the potential to achieve significantly greater earnings growth.

• Niche leaders. Many small and micro-cap companies are leaders in their chosen business niche, dominating specialised markets, which can give them pricing power.

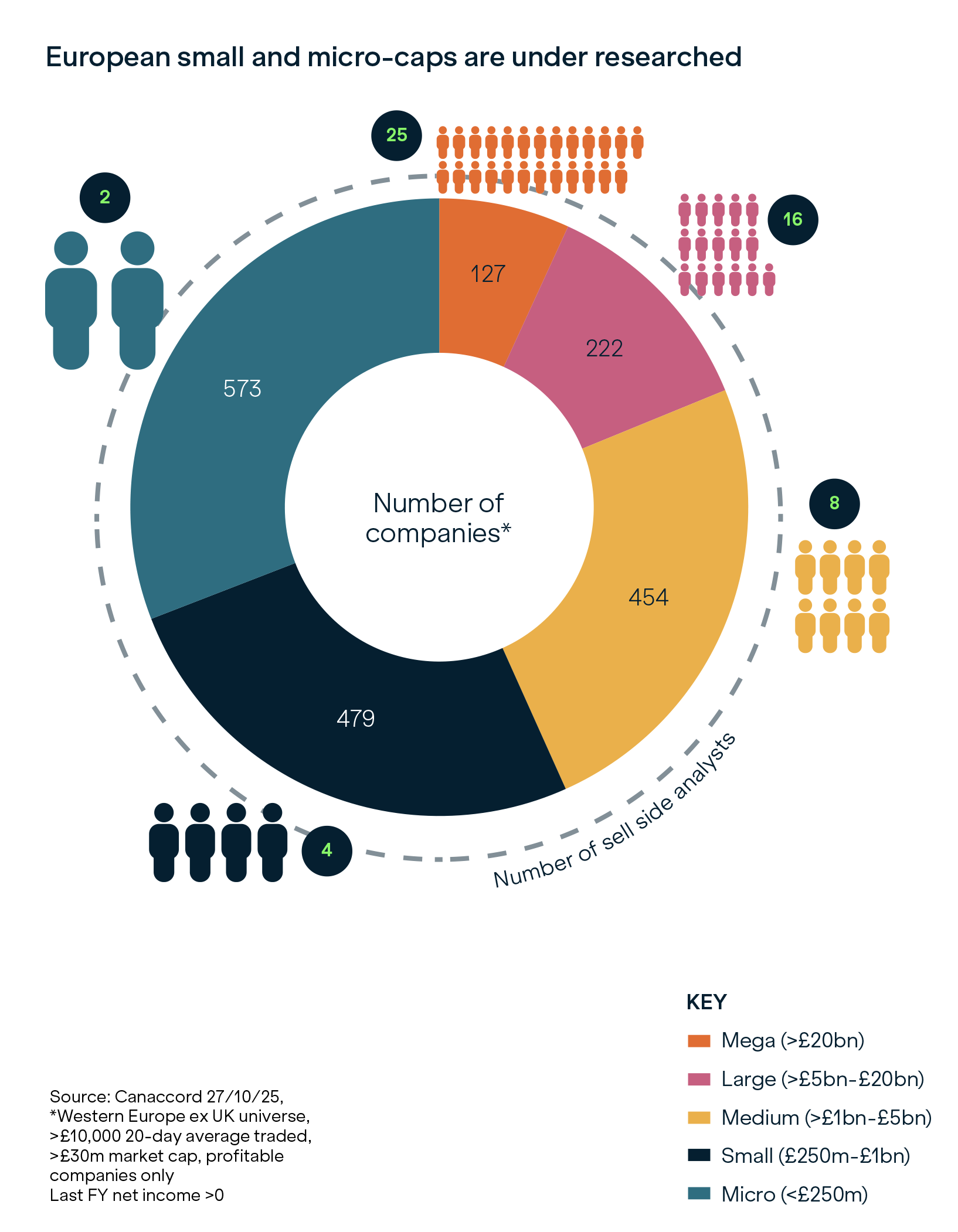

In addition, small caps tend to be under-researched compared to larger companies, which creates opportunities for specialist stock-pickers to identify opportunities overlooked by the wider market. There are simply fewer analysts and fund managers looking at the lower end of the market cap spectrum.

An average of 16 sell-side analysts are looking at each European large-cap company – and its around 25 for each mega cap. But only around four analysts are looking at each small-cap stock and two at each micro-cap stock.

• Lower interest rates. The European Central Bank (ECB) cut interest rates to 2% last year and has held them steady since. Small caps have historically tended to outperform large caps after interest rate cuts.

Small caps have historically tended to outperform large caps following interest rate cuts.

One reason for this is that small caps are typically more reliant on bank borrowing for growth and operational financing than large caps.

They also often face higher interest rates. Cuts to interest rates reduce borrowing costs and this can improve their profitability and growth prospects by, for example, lowering the cost of debt to finance capital expenditure.

• Moderating inflation. Inflation appears to have settled around the ECB’s 2% target, boosting consumer confidence, which is likely to mean increased spending.

• Stable economic growth outlook. The International Monetary Fund’s forecast is for modest but stable economic growth in the eurozone, with GDP expected to have increased by 1.2% in 2025 and predicted to rise by 1.1% in 2026.

At a time of heightened geopolitical tensions and new trade tariffs, the fact that small and micro-cap companies tend to be more focused on domestic markets means they also tend to be less exposed to these headwinds.

While small and micro-cap companies can be more volatile and less liquid, we believe the combination of attractive valuations, signs of a performance turnaround, superior earnings growth forecasts, structural advantages and a positive macroeconomic backdrop have created a compelling opportunity in European small-cap and micro-cap equities.

Only around 7%* of assets under management in European equity funds are invested in smaller companies, which provides significant scope for reallocation by institutional investors.

The IFSL Marlborough European Special Situations fund employs a multi-cap approach, with a bias to small and micro-caps.

The experienced team invest in undervalued, well-managed companies with above-market growth potential.

The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting investments. The portfolios will be exposed to stock markets and market conditions can change rapidly. Prices can move irrationally and be affected unpredictably by diverse factors, including political and economic events.

This material is for distribution to professional clients only and should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such. Calls will be recorded for training and monitoring purposes.

Issued by Marlborough Investment Management Limited, authorised and regulated by the Financial Conduct Authority (reference number 115231).

Registered office: Marlborough House, 59 Chorley New Road, Bolton, BL1 4QP. Registered in England No. 01947598.