View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

I was cycling through a park on the way to work last week and noticed something unusual. The sun.

After weeks of rain and grey skies in the UK, there it was breaking through the mist. It got me thinking about the allotment and what to plant this year. A few warmer mornings can make you feel like spring has arrived. But anyone who’s spent time in a garden knows better.

One warm spell doesn’t mean the cold snaps are over. Plant too early, and you ruin the crop. Wait too long, and you miss your chance. And that’s pretty much where the Federal Reserve (also known as ‘the Fed’) finds itself today.

In short, the US central bank is in a bit of a pickle. It kept interest rates on hold last week, which everyone expected. But the interesting part is what comes next. The Middle East conflict is likely to push up inflation. The big question is by how much. Oil prices have risen sharply. And naturally, people are starting to ask if interest rates could actually go back up again.

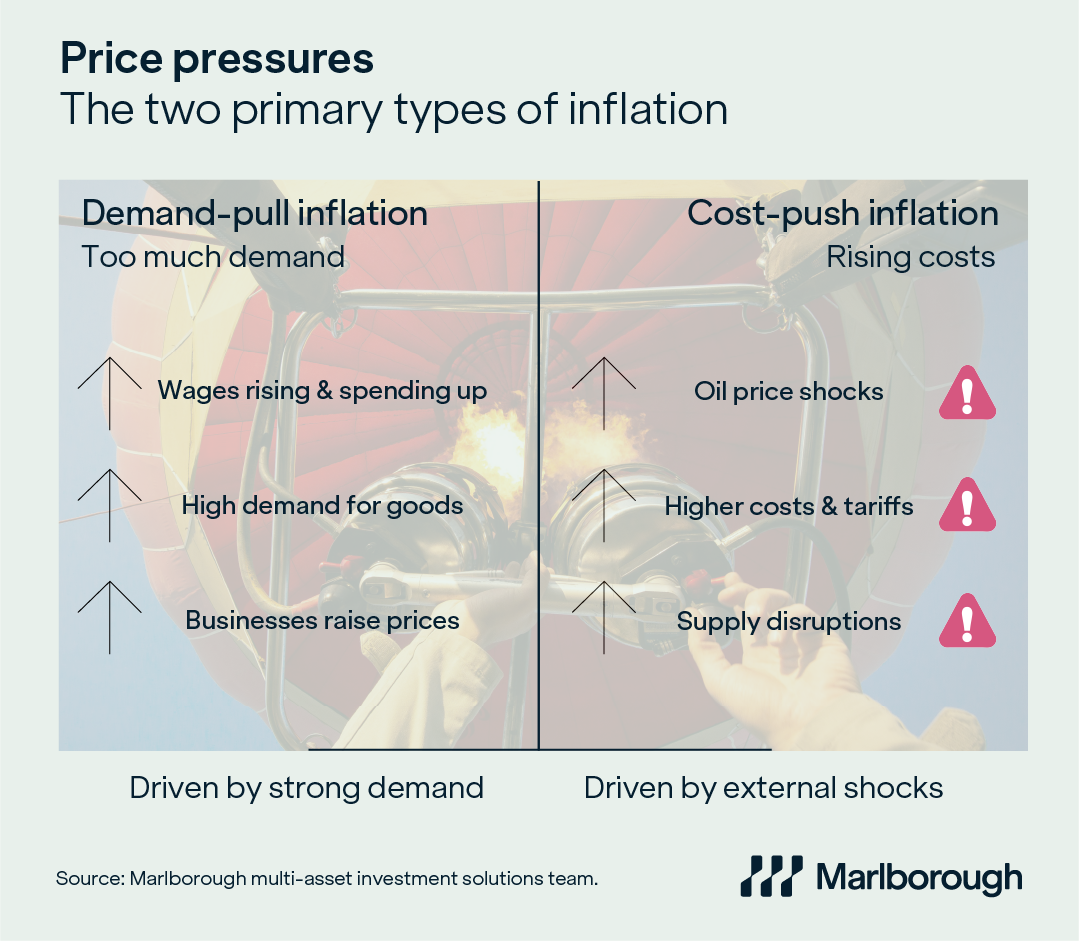

At this point it’s probably worth a quick recap on inflation, of which there are broadly two types;

• Demand-pull inflation – which is driven by strong demand. People are spending freely, chasing goods and services and pushing prices higher.

• Cost-push inflation – which is driven by rising prices. This is when prices rise because of a shock, when something suddenly gets more expensive, like oil.

Right now, what we’re seeing is much more the second type of inflation. It’s not that consumers are suddenly going on a spending spree. It’s that an external shock is nudging prices higher. And the Fed knows this.

When inflation is driven by strong demand, central banks tend to step in quickly and raise interest rates to cool things down. But when it’s coming from an external shock, like a sharp increase in energy prices, it’s a different story. Raising interest rates doesn’t produce more oil. So instead, the Fed is signalling that it’s likely to look through these short-term bumps, rather than reacting aggressively.

That means it's not likely to hike rates again. If anything, the overall direction of travel is still likely to be gently down, just perhaps not as quickly as investors had previously hoped.

Bond prices have fallen and yields* have risen. This has a lot to do with fading expectations of multiple bank interest rate cuts, which would have made the fixed income paid by bonds more attractive.

At times like this, it’s sensible to focus on the bigger picture – and the story is still broadly the same:

• Inflation is expected to ease, just not as smoothly.

• Economic growth is slowing, but holding up.

• Interest rates are likely to remain on a path downwards, although we may have to wait longer for cuts.

That’s not a bad backdrop. It’s just not a perfect one either.

Reacting to every short-term move in inflation or interest rates is a bit like planting your entire crop of vegetables after one warm day on the allotment. It feels right in the moment, but it rarely works out for the best. The experienced approach is to take your time, watch the conditions and act gradually. Investing works the same way.

The Fed may be in a bit of a pickle, but investors don’t need to be. Not all inflation is created equal. And right now, central banks are dealing with short-term price bumps, not an overheating economy.

This means the bigger risk isn’t what the Fed does next. It’s overreacting to what we think it might do. Whether it’s planting or portfolios, a patient approach is likely to serve us better for the long term.

*Yield is the income paid by bonds or other investments. It is usually stated as a percentage of the value of the investment

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.