View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

I’ve got a simple test for how the economy is really doing.

It’s not about gross domestic product (GDP) data or inflation forecasts. It’s whether your local restaurant is busy… and whether what’s on your plate looks the same as it did a year or two ago.

A number of clients have raised this recently, highlighting the Côte Brasserie chain of restaurants. They’re still full. The atmosphere is good. But portions don’t quite feel as generous as they once were. It’s a great real-world example of what’s happening beneath the surface of the UK economy.

On the face of it, things look fine. But dig a little deeper, and you can see the pressure. In the case of restaurants, that could be higher prices, subtle menu changes or smaller portions.

These real-world signs of economic stress fit with what we’re hearing from institutions like the International Monetary Fund (IMF) and the Organisation for Economic Co-operation and Development.

The message is consistent. Growth is holding up for now, but the outlook for the UK economy is weakening. UK Consumer Prices Index (CPI) inflation ticked up from 3.0% in February to 3.3% in March, driven almost entirely by fuel prices. The Bank of England has warned a prolonged energy shock could push inflation higher still.

Meanwhile economic growth is slowing. The IMF has cut its forecast for UK economic growth in 2026 to 0.8% (compared to its January prediction of 1.3%). This combination of weaker growth and rising inflation is what’s driving negative headlines.

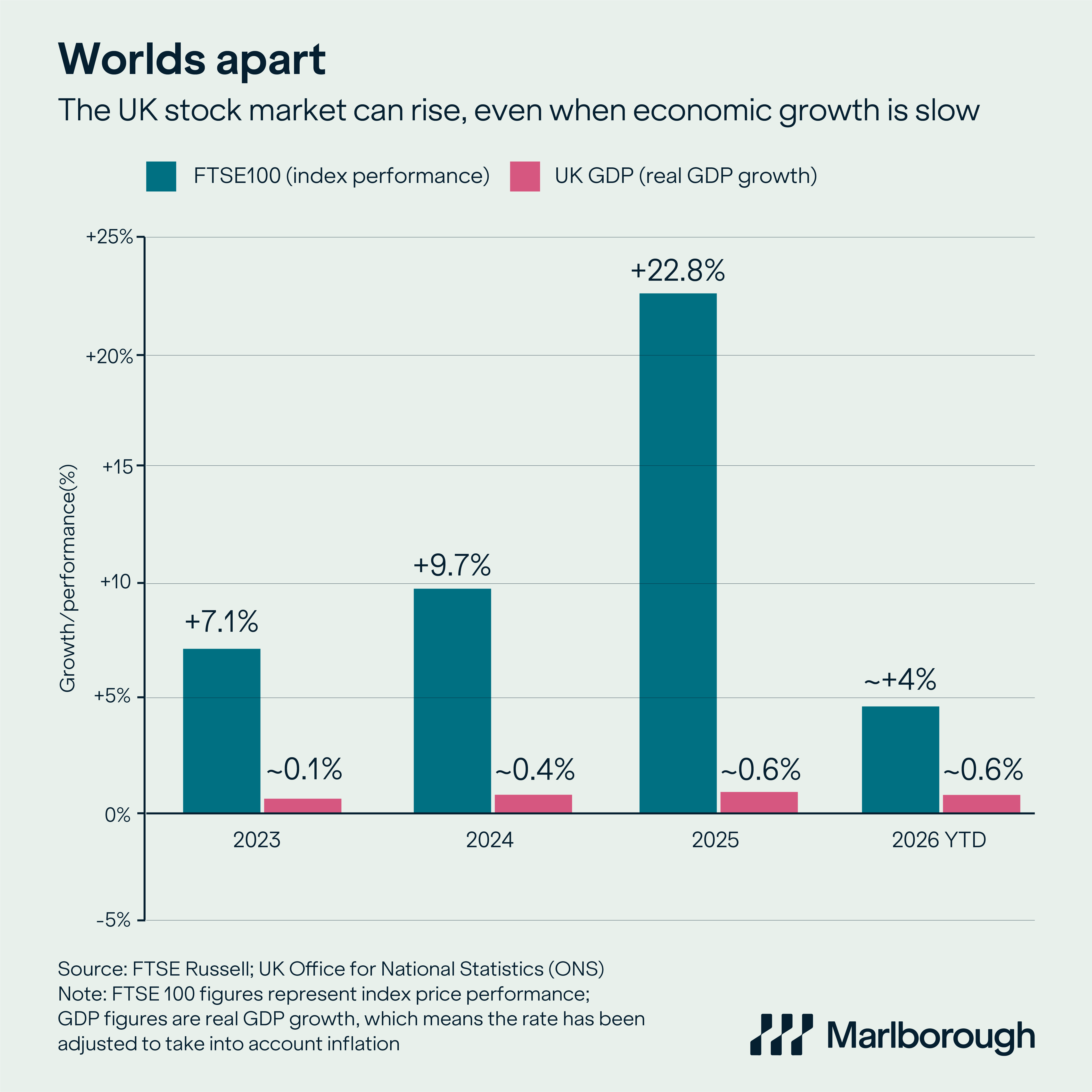

But the economy is not the stock market. It’s easy to assume that weaker growth leads to weaker markets. In reality, the relationship is far less direct. The FTSE 100 is a good example. As our chart shows, despite years of subdued domestic growth, it has delivered steady positive returns.

The reason is simple: most of the companies in the index are global businesses. Around three-quarters of FTSE 100 revenues are generated overseas. These companies are driven more by global demand, commodity prices and international trends than by the UK consumer. In fact, some of the very forces that are weighing on households, like higher oil prices, can boost earnings for some companies.

So while the UK economy may feel like it’s under pressure, the UK stock market has a different set of drivers.

To paraphrase veteran investor Warren Buffett, markets are forward-looking machines. Economies are slow-moving ones. And right now, that gap is on full display.

It’s important to distinguish between what’s driving inflation in the short term and what could keep it elevated. Energy tends to create short-term spikes. More persistent inflation tends to be fuelled by rising prices for services, driven by costs such as wages and rents. Services are the largest single component driving UK inflation and these prices move more gradually than, for example, energy and food. So while the oil price is dominating the headlines, it doesn’t necessarily define the long-term trend.

The experience of diners at Côte Brasserie is a microcosm of the broader economy. Demand is still there, and restaurants are busy. But costs for labour, energy and ingredients are rising for restaurants. Businesses are responding with smaller portions and subtle pricing changes. What we’re seeing isn’t a collapse in activity. It’s a gradual economic squeeze playing out in real time.

Weak economic growth doesn’t automatically mean weak investment returns. The UK economy may be feeling the pressure from higher energy costs and delays to expected interest rate cuts. But the companies most investors hold in their portfolios tend to be global in nature and influenced by very different forces.

You might notice the portion sizes getting smaller at the Côte Brasserie in your High Street, but the market isn’t just pricing in what’s happening in the UK. It's looking at portion sizes in New York and Hong Kong, too. This is one of the benefits of globally diversified portfolios. They provide exposure to economies around the world, helping us to manage risk and benefit from a much broader range of opportunities.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.