View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

As every parent knows, the school run is a burst of chaotic energy at the start of the day.

Have you filled the water bottles? Packed the books? Got the PE kit? Football today: boots and shin pads. And Spanish – that book’s needed too. And don’t forget snacks. Or coats.

All this while managing the inevitable meltdowns, navigating crowded pavements, waiting for the school gates to open and trying to arrive on time with a calm expression despite the chaos.

In many ways, January in financial markets has felt remarkably similar.

The first few weeks of the year have delivered a deluge of headlines demanding investors’ attention: the US seizing Venezuelan leader Nicolás Maduro; escalating protests met by violent crackdowns in Iran, prompting fresh sanctions and renewed talk of military action; US threats to take control of Greenland. Then, on top of all that, we’ve had White House proposals to ban institutional investors from buying single-family homes. And a mooted 10% cap on credit card interest rates.

Layer on top of that a weakening dollar, and it is easy to see why investors are feeling unsettled.

In noisy markets, the temptation is always to react. But just like the school run, most of the chaos is surface level. Beneath it, there is rhythm and structure, and there are patterns that repeat far more often than we realise.

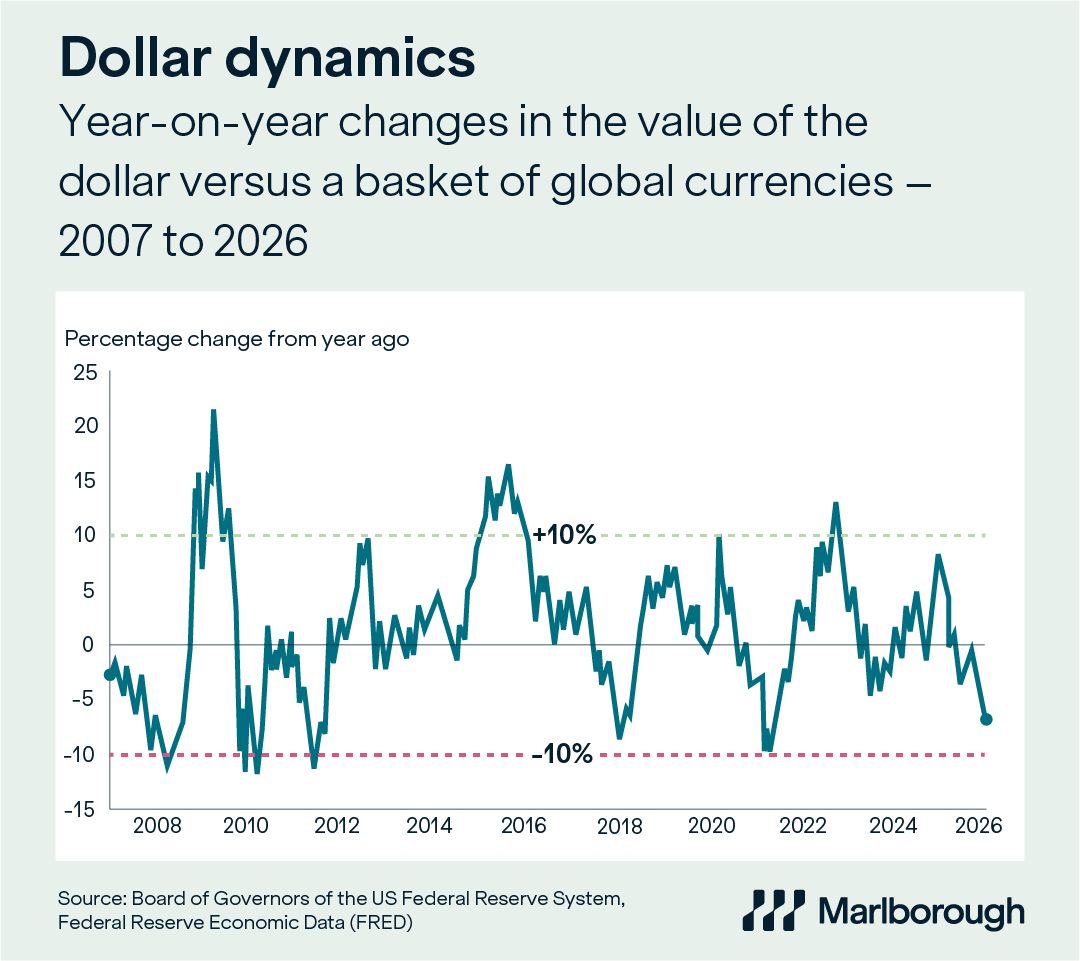

This week’s chart shows fluctuations in the value of the US dollar versus a broad basket of global currencies since 2007. The striking takeaway is just how normal swings are. Historically, the dollar routinely moves plus or minus 10% over a 12-month period. Episodes of perceived dollar weakness come and go with remarkable regularity.

Since the start of 2025, the dollar is down almost 9%* versus a basket of global currencies. That may feel uncomfortable amid today’s policy uncertainty, but it remains entirely consistent with historical norms.

For investors, this matters more than many realise.

Currency moves can meaningfully influence short-term returns. For UK investors, European equities delivered standout headline performance in 2025, but nearly 40% of that gain came from currency strength rather than underlying stock market performance. Strip out the currency effect, and European stock market returns were much closer to those of the US than many commentators acknowledge.

Currency also plays an important role in company profitability. Roughly 40% of the revenues of companies listed on the US S&P 500 index are generated outside the US. A weaker dollar increases the value of overseas earnings when they’re translated back into dollars. This is particularly significant for globally exposed business sectors such as technology, communications and raw materials.

In other words, dollar weakness is not automatically a negative. It often supports earnings growth and currency moves can boost the value of returns from other international stock markets. Most importantly, there is nothing historically unusual about what we’re seeing today.

The dollar continues to be underpinned by the size of the US economy, the scale of US financial markets, its dominant role in global trade and finance and the absence of any credible alternative as the dominant global currency. Headlines may come and go, but these foundations do not change overnight.

Like the school run, financial markets are a constant stream of noise, urgency and distraction. Our job is not to react to every wobble or stumble. It’s to stay focused, grounded and calm amid the storm, keeping our eyes firmly on the longer-term journey. Because most mornings, despite the chaos, the kids still make it through the school gates. And most market wobbles, despite the drama, resolve themselves in time.

*Bloomberg data to 28/01/26.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.