View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

Tomorrow marks the beginning of the Chinese New Year – and the arrival of the Year of the Horse.

If you’ve ever stood at the rails at Cheltenham or Ascot, you’ll know what the atmosphere’s like at a big horse race. The paddock buzzes. The horses shift with nervous energy. The jockeys try to keep the horses steady. The crowd revels in the atmosphere. And all the time, the favourites are attracting a lot of attention. But seasoned punters know something important. When the odds on the favourites shorten too far, the rest of the field starts to look interesting.

In Chinese astrology, the horse represents energy, drive, independence and movement. At times it also represents impatience. That feels rather like markets today.

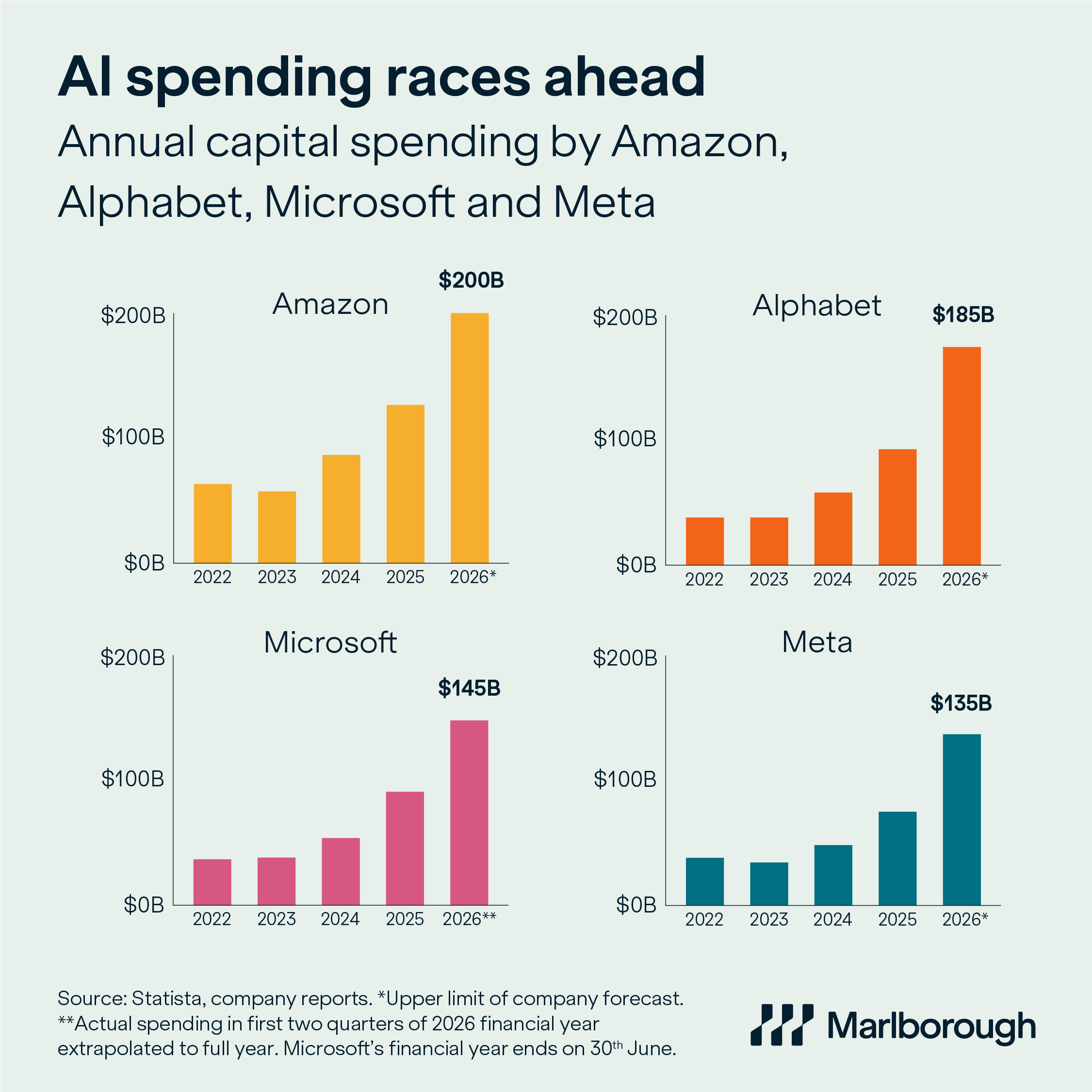

The US ‘hyperscalers’ – the tech giants operating massive networks of data centres that provide the computing power for artificial intelligence (AI) – have made their move, as our chart this week shows. It highlights four US technology giants and their expected capital spending this year, most of which will go on data centres and other AI infrastructure.

Amazon, Microsoft, Alphabet (Google’s parent company), Meta and Tesla are expected to spend a total of nearly $700 billion in 2026. That’s a huge increase on previous years’ spending. Amazon is likely to spend roughly $200 billion, Alphabet sits close behind at around $185 billion, Microsoft is expected to spend about $145 billion and Meta is likely to invest around $135 billion. Meanwhile, Tesla (not on our chart) is expected to spend $20 billion.

Last year, these four companies and Tesla generated close to $600 billion in operating cash flow. In 2026, most are expected to spend almost everything they generate on AI infrastructure. This is not a cautious approach. It’s full commitment. The favourites have gone off hard.

At the start of a big race, the favourite can look unstoppable. But once the first furlong passes, stamina and positioning begin to matter. So does price. Year to date, we are starting to see a subtle shift. It’s no longer only about the technology giants. Stock market performance is broadening out to other companies. Businesses more exposed to the economic cycle have come back into favour. Companies in the financial and industrial sectors are also contributing positively to stock market performance. And international stock markets are looking stronger. With the huge spending on AI infrastructure, the odds on the favourite, Big Tech, have shortened. Expectations are high. When that happens, investors naturally look elsewhere.

The hyperscalers can fund this investment. Their profitability is substantial. The question is not whether they can spend. The question is what return that spending will ultimately generate. The answer won’t be known this year. And until the picture is clearer, markets will continue to rotate and reassess. That’s not instability. It’s the race settling into its natural order. And as any experienced racegoer knows, it’s rarely wise to focus solely on the favourites when the field is wide and highly competitive, and the odds are shifting.

The Year of the Horse is about momentum and movement. Markets have both. The key is spreading your bets and letting the race unfold. Multi-asset investing is about spreading risk and backing a wider range of opportunities.

There are huge differences between a carefully diversified multi-asset portfolio and a horse race. But if you’re looking for a horse racing analogy, then we believe multi-asset investing is closer to the equivalent of an each-way bet, rather than a single all-out gamble.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.