View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

Over Christmas, one of the kids unwrapped a classic game: Battleships. Two grids. Hidden ships. And the slow, methodical process of probing the board, square after square, trying to work out where your targets are and what’s just empty ocean.

It turns out that’s a surprisingly useful way to think about today’s oil market.

Recent headlines have been full of stories about ships trying to beat sanctions and tankers being stopped or redirected, whether it’s linked to Russian exports or the latest developments in Venezuela. Traders and refiners are already positioning for potential new flows of Venezuelan oil. This comes after the Trump administration signalled it may take control of as much as 30-50 million barrels of Venezuelan oil, with talks underway on licences for companies like Chevron to operate in the country.

Meanwhile, Chinese oil companies are seeking guidance from Beijing on how to protect their investments in Venezuelan oil infrastructure. The practical upshot is that a lot of nervous energy is being used to try to work out where the next barrels might come from, much like scanning a Battleships grid for that elusive cruiser.

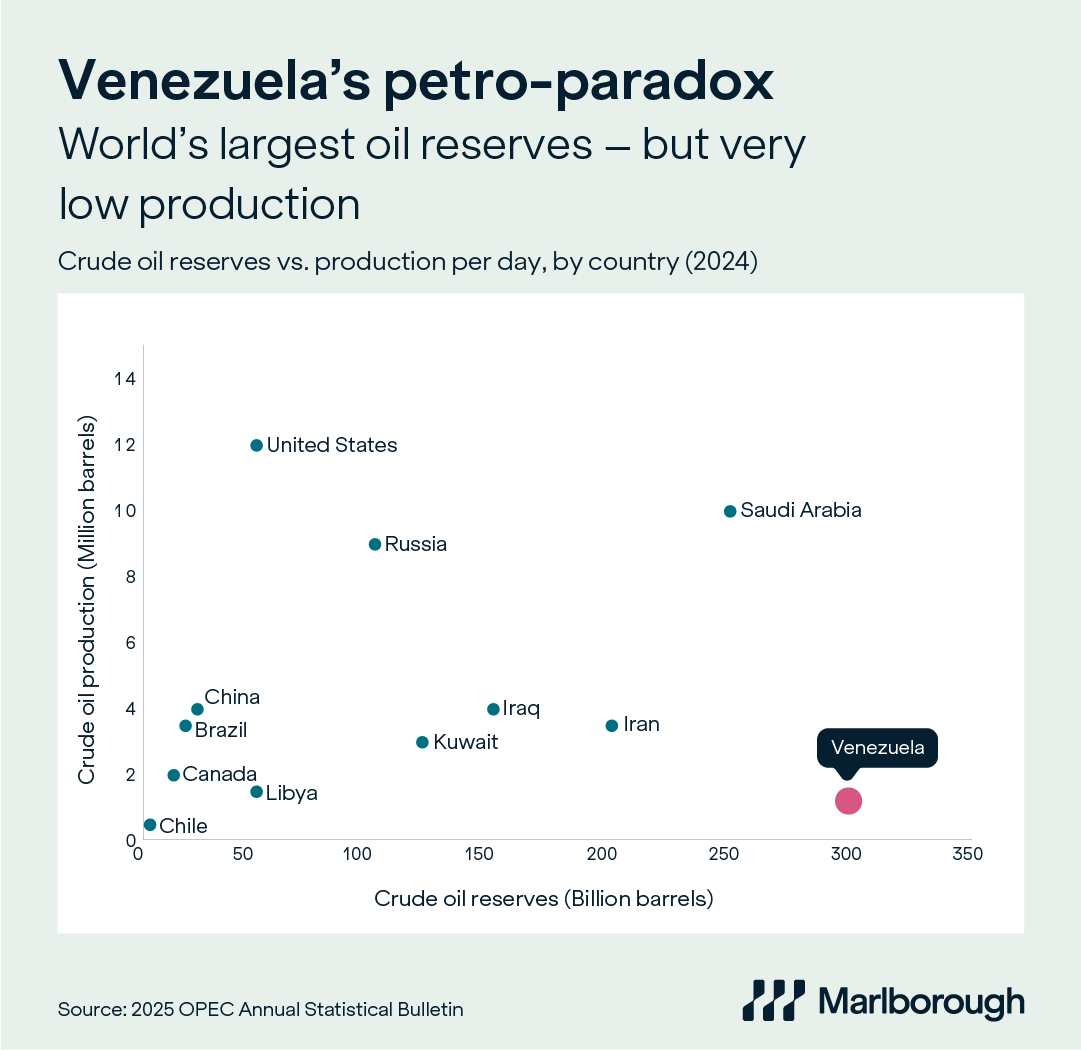

Our chart this week highlights a stark disconnect: Venezuela holds the world’s largest proven oil reserves (over 300 billion barrels) yet its current production sits below one million barrels per day, a fraction of its historic scale. On paper, Venezuela is an oil superpower. In practice, it’s a marginal producer with severely degraded infrastructure after years of underinvestment.

The impact of the US intervention on oil prices is likely to be modest in the near term, although it could be more significant over the longer run, according to analysis by Goldman Sachs. It looked at the expected impacts on the two main oil benchmarks, Brent Crude (which is used for the oil market in Europe, Africa and the Middle East) and West Texas Intermediate or WTI (which is used for the US oil market).

The investment bank forecasts that the most likely scenario for 2026 is that the price of a barrel of Brent Crude will average around $56 and WTI will average around $52. In this scenario, Venezuelan production lingers near current levels rather than surging.

Goldman Sachs has outlined two other possible scenarios. If Venezuelan production rises modestly – by around 400,000 barrels per day – average prices this year for both Brent Crude and WTI could be around $2 lower per barrel. On the other hand, if production falls – due to renewed disruption, sanctions bottlenecks or storage constraints – prices could be around $2 higher.

These relatively modest price impacts reflect how markets are currently interpreting events in Venezuela. The reason the oil market hasn’t moved sharply up or down is simple – the implications of the US intervention remain unclear, but any impact on supply is likely to be gradual, not sudden and seismic.

Over the longer term, the effects will depend on a range of factors, including infrastructure rebuilding, sanctions policy and the level of new investment. Markets have reacted calmly to the US intervention because, as things currently stand, we’re looking at a range of modest outcomes rather than a binary event with a sudden and dramatic impact.

It’s easy to overreact to every headline and every geopolitical twist, assuming the board has changed. But markets care about confirmed hits, not hypothetical ones. Venezuela could one day have the biggest oil tankers on the board. But for now, they’re still largely stationary, and Venezuela’s production is unlikely to move oil prices sharply in the short term. Instead, the real effect is likely to lie in the gradual realignment of long-term supply potential, which is something investors will be watching closely over the months and years ahead.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.