View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

On a recent flight, I was struck by a subtle but telling change in the cabin layout. The number of first-class seats was noticeably larger than on comparable routes in previous years, while the economy cabin (where my seat was) appeared more compressed. Airlines, like all businesses, respond to demand. This shift in configuration reflects a broader economic reality.

Over recent years, we’ve seen what is often described as a ‘K-shaped’ recovery. Households with assets such as shares, property and pensions have generally benefited from rising asset prices, while those without assets have faced a very different experience. Higher inflation has driven up the cost of living, eroding purchasing power and placing greater pressure on households reliant on income rather than capital.

The result is a widening divergence in outcomes. Those on the upper arm of the ‘K’ have seen their wealth grow, while those on the lower arm have felt increasingly under pressure. It’s little surprise then that companies are targeting consumers with greater spending power. Demand for premium goods and services is continuing to grow, even while some are struggling to balance their household budgets.

This backdrop provides a useful lens through which to view current policy discussions in the US, as attention begins to focus on the build-up to the US midterm elections in November. All 435 seats in the House of Representatives and a third of the seats in the Senate will be up for grabs.

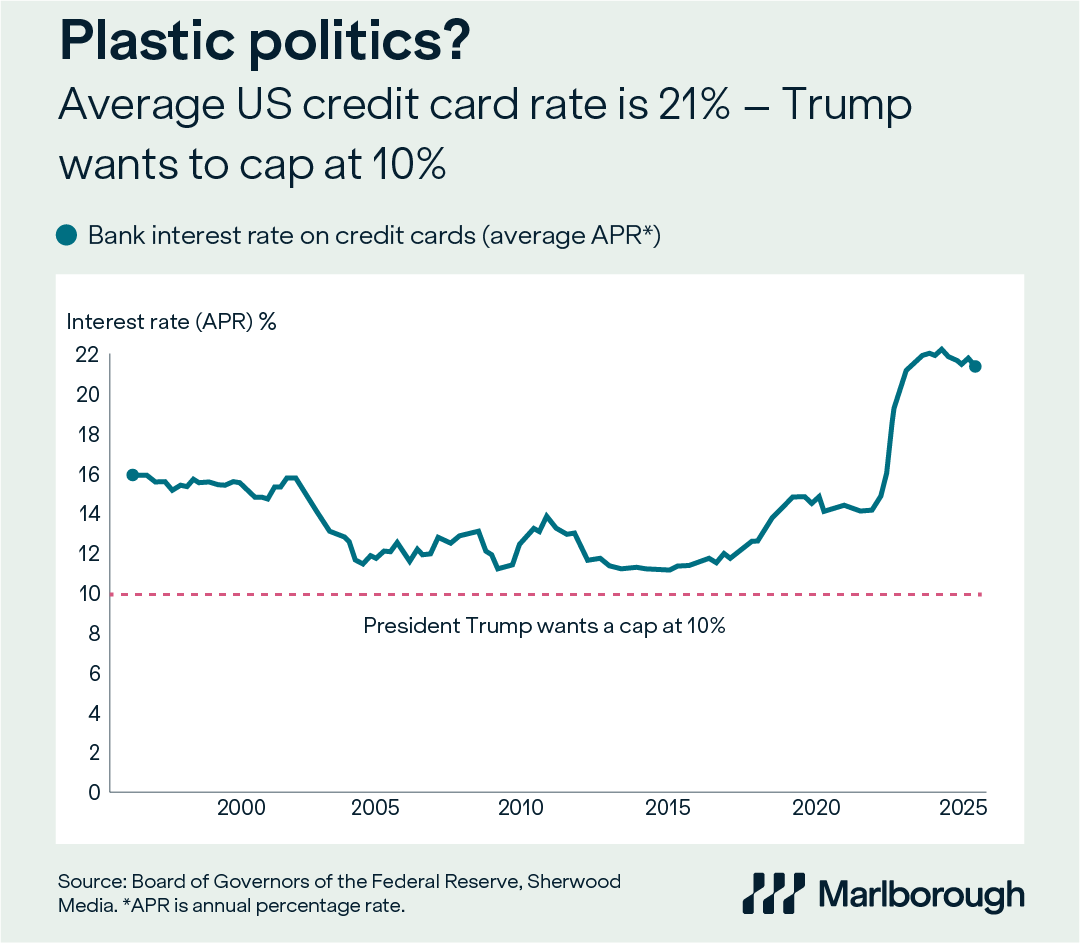

In preparation, President Donald Trump is increasingly leaning into voter-friendly economic initiatives. One proposal attracting particular attention is a suggested one-year cap on credit card interest rates at 10%, significantly below today’s average rate of around 21%.

From a political perspective, the appeal is clear. In a K-shaped economy, policies aimed at easing the burden of high-cost debt resonate most strongly with households on the lower arm of the recovery. Financial markets, however, have been far less enthusiastic. Investors have focused on the potential impact on profitability and credit availability, with companies directly in the line of fire. Card networks and consumer lenders (think Visa and Mastercard) have seen their share prices fall as investors digested the proposal.

Whether the policy will ultimately progress through Congress remains uncertain, but the proposal underlines how affordability, debt and financial pressures are becoming increasingly central themes as the midterms approach.

The K-shaped recovery continues to shape economic outcomes. Those with assets have generally benefited from rising markets and compounding returns, while those without assets have faced the full force of higher inflation and rising borrowing costs.

In this environment, accumulating assets and managing finances effectively has never been more important. Long-term financial progress is rarely about short-term policy announcements or market noise. It’s about having a clear plan, a disciplined investment approach and assets working efficiently over time.

That’s why professional financial advice is so important. A financial adviser can help their clients navigate complexity, make informed decisions and align their investments with long-term goals – not just for today, but for future generations as well.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.