View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

As an Irishman, it’s probably no surprise that one of my staple foods is Kerrygold butter. However, over the past couple of years, it’s begun to leave a bit of a bad taste in my mouth. Not because of the flavour, but because of the price.

Not so long ago, I could pick up a pack for about £1.90. Today, it’s closer to £3.00. Recently I spotted it for £2.50 and thought I’d lucked out, until I noticed the pack had quietly shrunk. Classic shrinkflation.

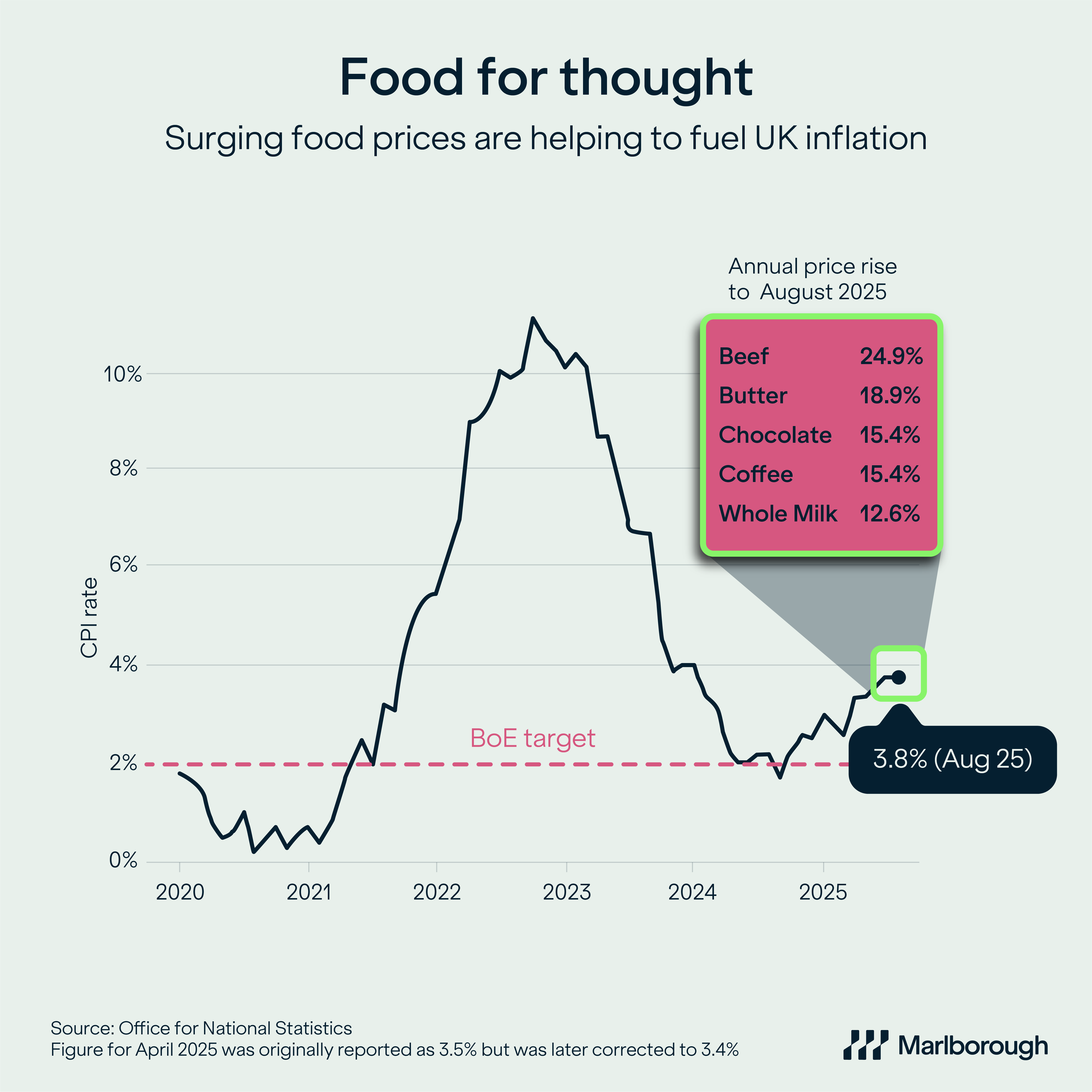

This small example highlights a much bigger issue. Food price inflation has been one of the most persistent and painful drivers of overall UK inflation. While headline inflation held steady at 3.8% in August, food prices climbed from 4.9% to 5.1%. It was their fifth consecutive monthly rise, and the highest rate of increase in 18 months.

Our chart shows how, after easing to the Bank of England’s 2% target last year, Consumer Prices Index (CPI) inflation has climbed again to 3.8%. It also shows examples of surging food prices that have contributed to the overall inflation rate.

Why is UK inflation remaining stubbornly high? Part of the answer lies in seasonal quirks: summer air fares and hotel prices (helped along by Oasis reunion gigs!) pushed inflation higher earlier in the year, before easing in August. But food inflation is being shaped by deeper pressures. As an allotment holder, I have some first-hand experience of how the weather plays its part. The UK just experienced a spring and summer that were among the hottest on record. This was great for holidaymakers, but not for farmers. It reduced crop yields and was a factor contributing to another below-par harvest, on the back of a rain-affected 2024 yield.

On top of this, food producers face rising costs in the form of higher wage bills, increased employers’ National Insurance contributions and other bills climbing, such as packaging tax. All of this feeds through to increases in the price of essentials like butter and milk.

The good news is that core inflation, which strips out food and energy, actually eased to 3.6% in August. Seasonal pressures will fade, and not every harvest is a disaster. A hot year followed by a wetter one can reverse supply shortages and ease prices. But for now, food inflation remains stubbornly high, which is making the Bank of England more cautious about interest rate cuts. That means rates may stay higher for longer, which has important implications for us, as multi-asset investors. It reinforces our view that a highly selective approach is needed when identifying the right bond funds for our portfolios.

Source of inflation data: Office for National Statistics

Find out more about our multi-asset solution

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.