View

Multi-Asset

Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.

By selecting intermediary or institutional investor I confirm that I am a financial professional and understand that the information should not be distributed to or relied upon by any other persons. It’s provided for general information purposes only and is not personal advice to anyone to invest in any fund or product. Information taken from trade and other sources is believed to be reliable, although we don’t represent this as accurate or complete and it shouldn’t be relied upon as such.

Last weekend my daughter took a tumble off her scooter and grazed her leg. After a few days, it was time to take off the plaster. Anyone with young children knows this moment isn’t really about pain… it’s about fear of the pain. The anticipation is always worse than the reality. As I tried to reassure her, “It’s fine, it won’t hurt, don’t worry”, my wife swiftly ripped the plaster off there and then. No countdown, no build-up, just done. My daughter looked at me, a little shocked, but mostly relieved. It wasn’t nearly as bad as she expected.

And that brings us to last week’s UK Budget.

In the run-up, markets braced for painful tax increases or spending cuts as the government tries to balance the public finances. The build-up was full of warnings. But when Chancellor Rachel Reeves finally delivered the Budget, the immediate reaction was oddly calm. Markets barely moved. The plaster came off… and it didn’t hurt. Not yet.

But here’s the catch. The headline tax rises are limited for now – many of the measures announced don’t bite today. Instead, they’re scheduled to take effect further down the line. This means taxes will rise over time, even if they don’t feel painful today.

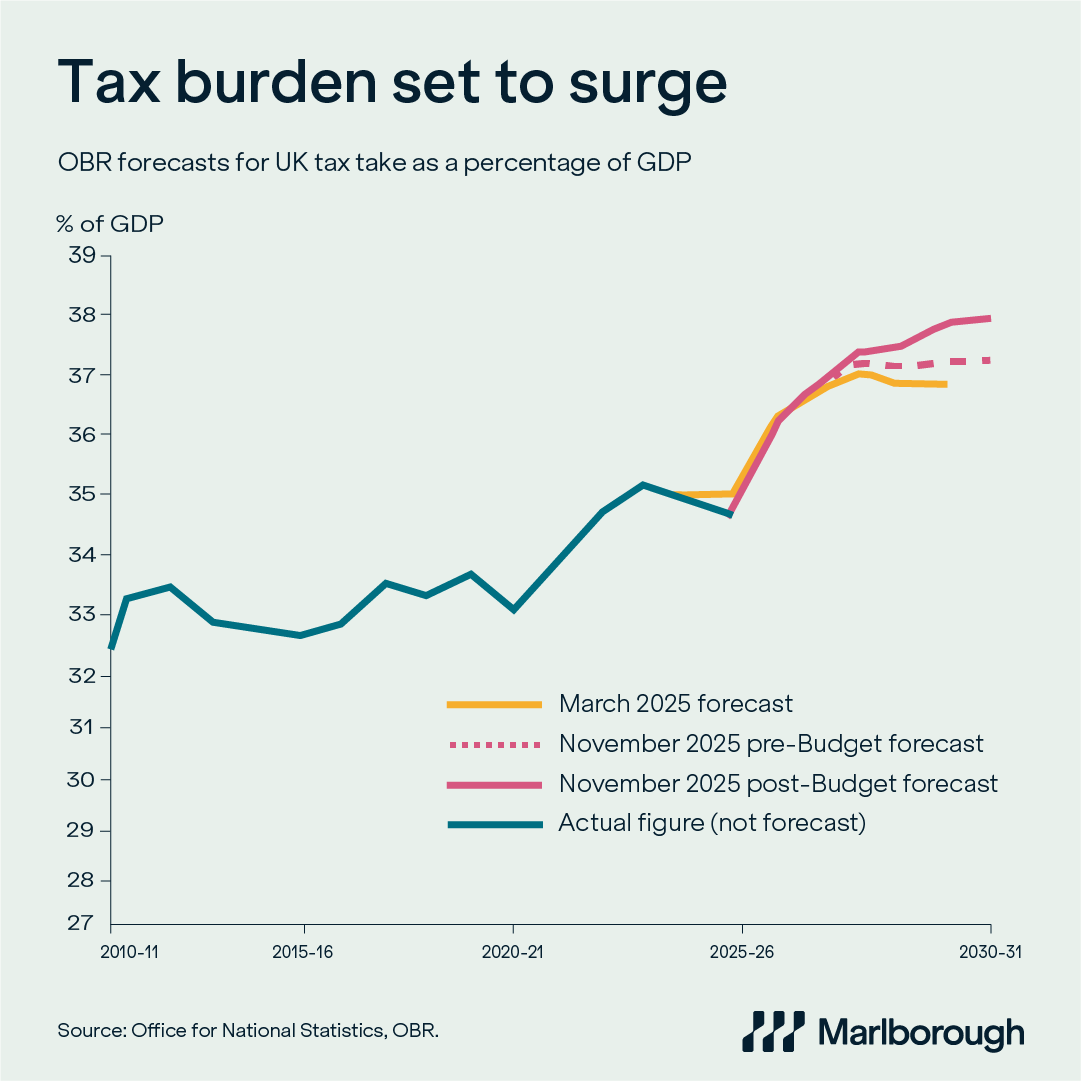

This week’s chart shows forecasts by the Office for Budget Responsibility (OBR), which provides independent analysis of the UK’s public finances. The forecasts are for the total of taxes levied (the tax take) as a percentage of the country’s economic output (as measured by gross domestic product or GDP).

After crunching the Budget numbers, the OBR expects the total tax take to increase from 34.7% of GDP in 2024-25 to 38.3% of GDP in 2030-2031. This forecast (the solid pink line) is significantly higher than the OBR’s forecast in March (solid yellow line), and their prediction earlier in November before seeing the measures in the Budget (broken pink line).

The 38.3% level forecast for 2030-2031 would be a historic high and is 5.4 percentage points higher than the pre-pandemic level of 32.9% in 2019-20.

The tax changes announced in the Budget include:

• An extension of the freeze on Income Tax thresholds, which is a ‘stealth’ tax increase. If these thresholds don’t rise to keep pace with inflation, then more people will pay higher tax rates, even though their spending power hasn’t increased in real terms.

• Higher tax rates on income from dividends, savings and property will hit investors, landlords and anyone earning from non-employment income. This is a clear signal the Budget is leaning on wealth and investment income rather than wages.

• The new ‘mansion tax’ on properties worth over £2m and changes to salary sacrifice rules affecting pension contributions target wealthier households or those saving heavily for retirement. Again, this shifts the burden to those with more capacity to pay or higher wealth.

Taken together, the measures suggest the government wants to significantly increase revenues over time, while avoiding the headline shock of raising Income Tax or VAT.

Markets breathed a sigh of relief after the Budget, but our focus is on what comes next. Although the measures don’t bite immediately, a series of delayed tax changes will gradually influence how much households and businesses have to spend. Over time, higher taxes can act as a headwind to growth. This is something we’ll be monitoring closely as we manage investment portfolios.

What makes this Budget unique is its patchwork approach: many smaller, delayed measures affecting different people in different ways. This means the impact won’t be felt all at once, and it won’t be the same for everyone.

From an investment perspective, we’ll continue to assess how these changes may influence economic growth, consumer spending and ultimately markets. Given the variety of changes ahead, it may also be a good moment for individuals to check in with their financial adviser to understand what the Budget could mean for them personally.

This article is provided for general information purposes only and should not be construed as personal financial advice to invest in any fund or product. These are the investment manager’s views at the time of writing and should not be construed as investment advice. The opinions expressed are correct at time of writing and may be subject to change. Capital is at risk. The value and income from investments can go down as well as up and are not guaranteed. An investor may get back significantly less than they invest. Past performance is not a reliable indicator of current or future performance and should not be the sole factor considered when selecting funds.